The Art of Long-Term Wealth Multiplication: A Practical Guide to Reaching True Financial Autonomy

Financial Freedom ,Long term wealth creation ,personal finance , Financial Growth, The Compounding Phenomenon, Art of Portfolio Balance

What is Goal-Based Investing ? Many of us envision a future where money ceases to be a source of daily anxiety. Whether your personal milestone looks like owning an organic orchard in a peaceful valley, securing a modern penthouse in a thriving metropolitan area, or retiring early to travel the globe, making these aspirations a reality requires a deliberate shift toward expanding your net worth.

However, it is easy to mistake a comfortable monthly paycheck for actual wealth. True financial resilience is not determined by the size of your base salary. Instead, it is born from your ability to consistently redirect your surplus earnings into productive assets that work for you around the clock.

This guide clarifies the mechanics of sustainable wealth accumulation, explains why it remains essential for your future stability, and outlines practical investment approaches with visual tools to help you systematically hit your milestones.

1. Demystifying Wealth Creation–Goal-Based Investing

Strip away the complex financial jargon, and wealth creation is simply the disciplined act of allocating your surplus capital into diverse financial tools over an extended timeline to construct a dependable financial cushion. It is the transition from depending solely on active income (trading your hours for dollars) to cultivating passive income (allowing your accumulated capital to generate new revenue).

To understand your true financial standing, look at this fundamental balance sheet calculation:

Net Worth = Total Assets -Total Liabilities

The Anatomy of Net Worth

| Asset Category (What You Own) | Liability Category (What You Owe) |

| • Equity Stocks & Mutual Funds • Real Estate & Properties • Gold & Precious Metals • Fixed Deposits & Cash Reserves | • Outstanding Home Mortgages • Vehicle & Car Loans • Educational/Student Loans • Short-Term Credit Card Debt |

| Goal: Maximize Growth & Yield | Goal: Systematic Elimination |

Genuine wealth expansion takes place when the value of your assets climbs at a pace that far exceeds your liabilities. Ultimately, it matters very little how much capital passes through your hands each month; what matters is the portion you retain and successfully deploy into the economic ecosystem.

2. The Core Engines of Financial Growth

Building long-term wealth depends on three foundational engines. Neglecting any of these components makes it incredibly difficult for your portfolio to outpace rising living costs or achieve meaningful growth.

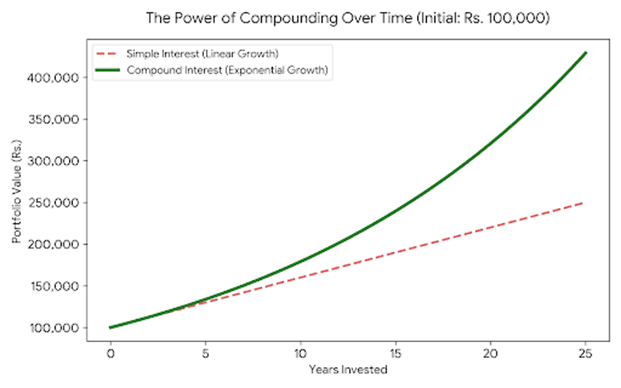

Engine 1: The Compounding Phenomenon

Compounding operates like a snowball rolling down a hill. The earnings produced by your initial capital are folded back into the principal, allowing you to generate returns on top of previous returns. In the opening years, the growth often feels minimal and slow. Over a multi-decade timeline, however, the curve shifts into a near-vertical trajectory.

As the chart illustrates, while a standard linear path (Simple Interest) plods along predictably, compounding interest gains incredible momentum as the years stack up. This illustrates an undeniable truth: time is your most potent ally in the market. The sooner you leave your investments alone, the faster they multiply.

Engine 2: The Early Investor Advantage

Because compounding requires an extended runway to unleash its full potential, launching your investment plan early gives you an extraordinary head start. Consider how much a delay changes your trajectory:

| Metric | The Early Starter (Age 25) | The Delayed Starter (Age 35) |

| Monthly Investment | Rs. 10,000 | Rs. 20,000 |

| Duration until Age 60 | 35 Years | 25 Years |

| Total Out-of-Pocket Invested | Rs. 42,00,000 | Rs. 60,00,000 |

| Estimated Corpus at 12% p.a. | ~Rs. 6.49 Crore | ~Rs. 3.79 Crore |

Despite investing double the monthly amount, the delayed starter ends up with roughly Rs. 2.7 Crore less at retirement, simply because they missed out on 10 years of early compounding.

Engine 3: The Systematic Capital Step-Up-Goal-Based Investing

As your professional skills grow, your income will naturally scale up through promotions, job transitions, or corporate bonuses. The hidden enemy here is “lifestyle creep”—the habit of inflating your everyday spending at the exact same rate as your earnings.

To supercharge your financial timeline, apply a step-up mechanism to your savings. Whenever you receive a 10% bump in pay, immediately adjust your automated mutual fund contributions or Systematic Investment Plans (SIPs) upward by that same 10%. This minor modification dramatically shrinks the number of years you must work.

3. Why Cultivating Assets Matters

Keeping the deeper goals of asset accumulation fresh in your mind helps you stay steady when the stock market experiences its inevitable downturns. Building a robust portfolio serves several vital purposes:

- Buying Back Your Time: As legendary value investors observe, the true goal of building assets isn’t consumerism; it is autonomy. When your investments produce enough cash flow to offset your daily baseline expenses, professional work transforms into a voluntary passion rather than an economic obligation.

- Insulating Your Purchasing Power: Leaving your entire financial reserve sitting in a basic bank account quietly erodes your purchasing power due to inflation. If the annual cost of living increases by 5% to 6%, any capital yielding a lower return is actively shrinking in real terms. A properly structured wealth plan focuses heavily on growth-oriented asset classes like equities, which historically outpace inflation over multi-year cycles.

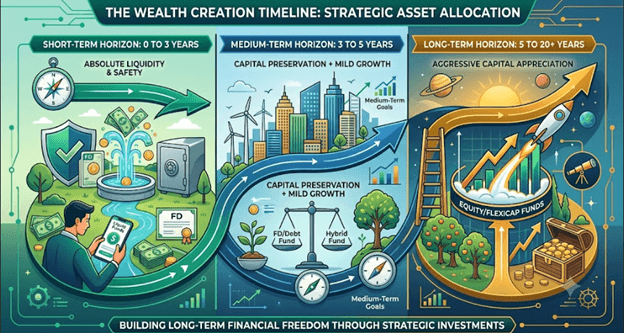

Categorizing Your Life Goals

Short-Term Horizon: 0 to 3 Years —>

Focus: Absolute Liquidity & Safety (Liquid Funds, FDs)

Medium-Term Horizon: 3 to 5 Years —>

Focus: Capital Preservation + Mild Growth (Hybrid/Debt Funds)

Long-Term Horizon: 5 to 20+ Years —>

Focus: Aggressive Capital Appreciation (Equity/Flexicap Funds

4. Matching Financial Vehicles to Your Timeline

A widespread misstep among risk-averse savers is prioritizing absolute capital safety for objectives that are decades away. While fixed-income choices are perfect for shielding money you need next year, leaning on them too heavily for long-term targets runs the risk of falling short of your target.

Consider a practical comparison. Suppose your objective is to accumulate a sum of Rs. 4 Crore over a continuous 20-year window.

If you opt for a conservative traditional Fixed Deposit (FD) yielding a steady 6% annual return, your principal remains insulated from market drops, but its growth rate is flat. On the flip side, if you select a diversified Flexicap Mutual Fund—which historical market averages suggest can generate a long-term return of roughly 12% annually, your wealth compounds significantly faster.

Monthly Outlay Required to Reach Rs. 4 Crore in 20 Years

| Asset Choice | Estimated Annualized Return | Investment Timeline | Required Monthly Outlay |

| 🏦 Traditional Fixed Deposit (FD) | 6.0% per annum | 20 Years | Rs. 86,150 per month |

| 📈 Diversified Flexicap Fund | 12.0% per annum | 20 Years | Rs. 40,035 per month |

Relying solely on fixed-income instruments forces you to set aside more than double the amount of out-of-pocket cash each month to hit the exact same target. By choosing equity-centric vehicles for your distant milestones, you allow market expansion to handle the heaviest part of the load.

5. Asset Allocation: The Art of Portfolio Balance

To survive economic downturns without losing sleep, your portfolio needs to be diversified. This means spreading your cash across distinct asset groups that react differently to changing economic cycles.

A resilient portfolio typically divides its weight among these primary buckets:

- Public Equities (Stocks & Mutual Funds): Serves as your primary growth engine over long horizons.

- Fixed Income (Bonds, PPF, or Senior Debt): Offers portfolio stability, curbs downside drops, and delivers predictable interest cash flow.

- Gold & Precious Metals: Acts as a safe-haven hedge when inflation spikes or global currencies devalue.

- Real Estate: Supplies tangible value, rental yield potential, and steady long-term appreciation.

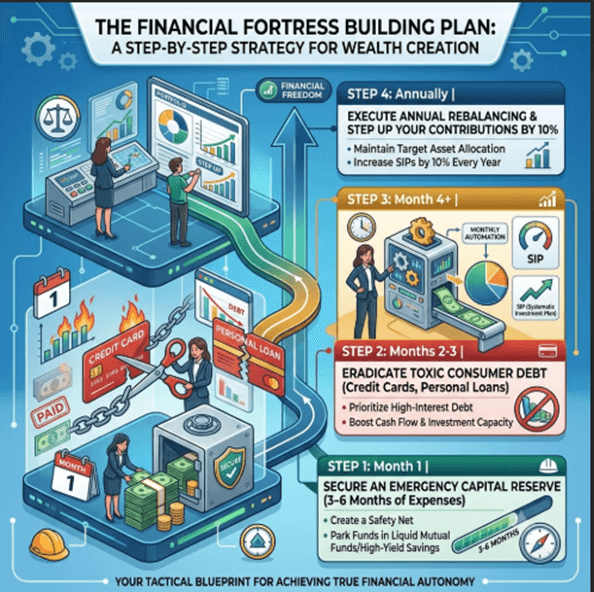

6. Your Tactical Roadmap to Wealth

If you are ready to transition from a passive saver into a strategic investor, use this structured, sequential blueprint to guide your choices:

The Golden Rule of Asset Management: Wealth accumulation is a marathon, not an afternoon sprint. It doesn’t require chasing highly speculative, overnight trends. Instead, true security is won through consistency, clear goal alignment, and the emotional discipline to allow your capital to compound over time.